PRLEXUS draws my attention after it crossed and closed above 200 days SMA on 7 april.

it had been falling down before the released of the disappointed 1QFY17 result, from 1.66 to 1.36

afterwards, it had been trading between 1.36 - 1.47 range even though the 2QFY17 result reported net profit rose 9% yoy. After a month of waiting, it successfully broke the strong resistance of 1.47 & 1.50 yesterday with volume, im now waiting for it to pull back to add more

|

| http://www.malaysiastock.biz |

|

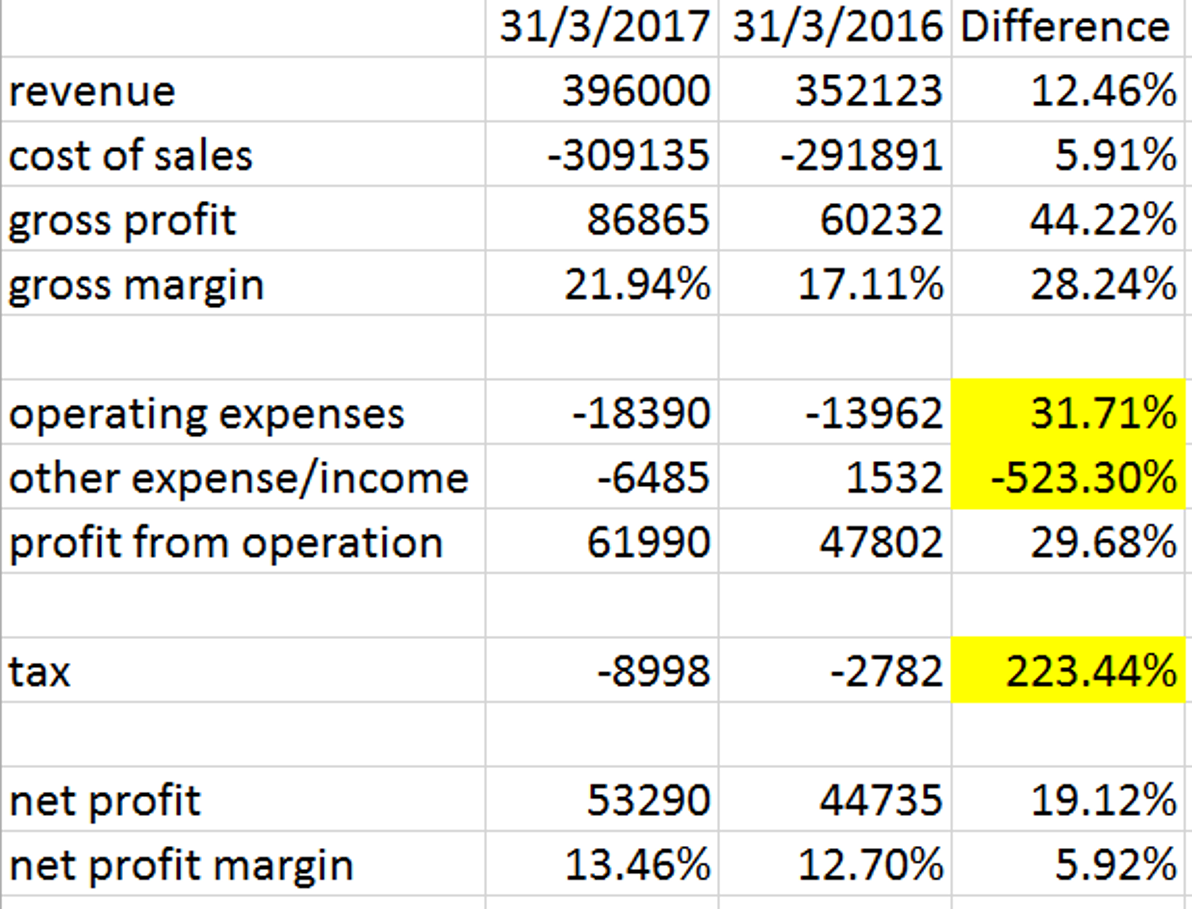

Revenue, net profit & profit margin increasing consistently year after year

High ROIC & ROE, net cash company, trading at PE of 10 & EBIT multiple of 4.73

|

Company Performance

Prolexus Bhd’s 1QFY17 net profit dropped16.7% yoy to RM6.4 m, mainly due to slower sales and probably the impact of minimum wages (from ww.wsinchew.com.my).

Fortunately, the performance rebounded as 2QFY17 result reported net profit increased 9% yoy mainly on higher contribution from the group’s apparel division

Apparel Segment -let’s just focus on Apparel since it accounting for 97% of the revenue

Apparels Manufacturing Business Unit

Prolexus Group has over the years established itself as one of the reputable garments manufacturer for the internationally renowned brands.

What are these renowned brands? Namely Nike, Oshkosh, Under Armour, ASICS, Gear for Sports, Champion, Fila, KRU, Disney, Umbro, Saks Inc, Parisian.

It has 3 manufacturing plants located in Malaysia and China to serve customer requirement. Prolexus is a garment designing and manufacturing service provider. Company products are exported to international markets which comprises of North American, European Union, Australia and Asia.

Apparels Retailing Business Unit

Prolexus has its own brands under Be Elementz and Bixiz Kids.

source:http://www.prolexus.com.my

Strengths & Opportunities

Profit margin

Gross margin held relatively steady at 19.2% (19.5% in 1HFY16). This was in spite of the full effect of higher minimum wage impact. Profit margin are expected to remain stable for FY17, given the cost-pass-through nature of Prolexus’ contracts.

New expansions

Meanwhile, Prolexus’ exciting double plant expansion remains on track to be completed in FY18. New Vietnam plant are anticitaped to commence operations in 1QFY18. It will initially enlarge existing output by 30%, with the potential to double existing capacity. Meanwhile, its Kluang fabric mill is scheduled to begin operations in 2QFY18. The fabric mill will enhance margins with cheaper knitted fabric input produced in-house. However, for the interim initial start-up costs and underutilisation of capacity are expected to initially weigh on margins (source: AmInvestment Bank Research)

Beneficiary of depreciating ringgit

According to its FY16 annual report, 97% of Prolexus’s FY16 revenue is contributed from exports to foreign countries, out of which the exports to US alone accounted for 55.5% of its revenue, whereas revenue from Malaysia accounts for merely 2.5%. Therefore, should ringgit continue to weaken, Prolexus will be rewarded with increasing foreign export demands as well as gains from foreign currency translation.

Source:http://aspire.sharesinv.com/38088/prolexus-slow-and-steady-wins-the-race/

Increasing demand for active wear

The growing demand for active wear around the world owing to increasing health awareness may attract new business opportunities to Prlexus

source:http://www.businesswire.com/news/home/20160831005048/en/Global-Sports-Fitness-Wear-Market-Witness-Growth

Weaknesses & Threats

90% of the group’s total sales are attributed to its key customers

About 65% of its sales for the year ended July 31, 2015 (FY15) were from Nike and another 25% were from Under Armour.

Source: http://www.theedgemarkets.com/my/article/prolexus%E2%80%99-vietnam-expansion-plans-boost-its-production-capacity

|

| source: http://www.sinchew.com.my/node/1599628/推行各种扩充计划.宝翔前景看俏 |

Revenue projection are lowered given the new development with Nike amid heightened competition from other brands such as Adidas and Under Armour (source: AmInvestment Bank Research).

Global economic downturn, geopolitical risks, intense competition that would be slowing down the business of its key customers, which in turn decreasing the orders

let's see who is the one that push up the price recently

|

| EPF and Manulife are buying!! |

Prlexus's products

Disclaimer: it isn't a buying recommendation, your money, your decision