|

| forecast P&L by TA Research |

let's get straight to the point

STRENGTHS & OPPORTUNITIES

Growing Automotive Segment

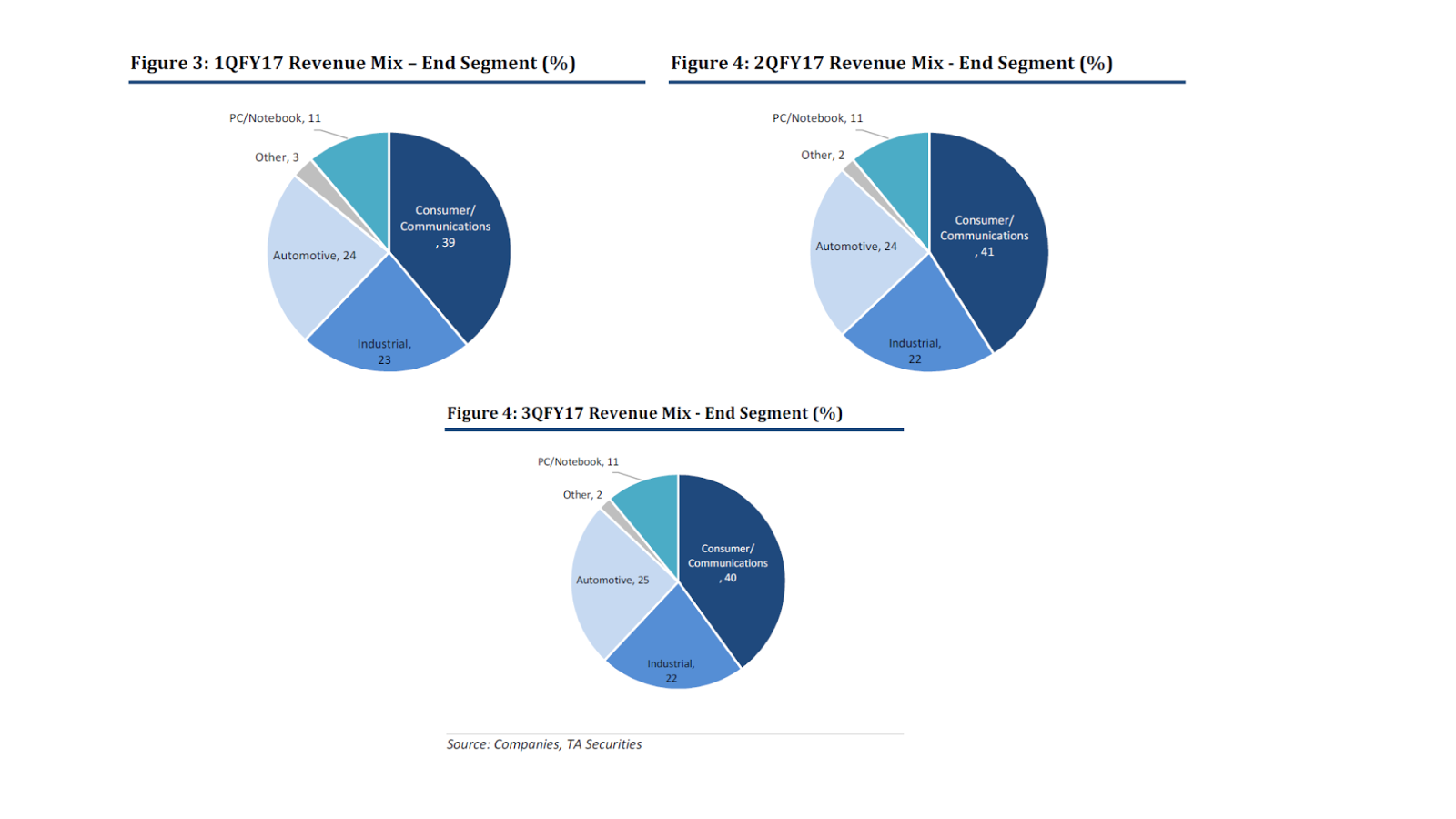

The global automotive semiconductor market is expected grow at a CAGR of 6.4% from 2017 to 2022. MPI is well prepared to grow its Automotive contribution from 24% of group revenue in FY16 to 50% over the next 2-4 years. Well positioned, MPI already has existing coverage of 7 out of the top 10 automotive suppliers (TA Research). MPI mentioned that leading Automotive technologies that are used for safety features have passed the stringent qualification stage and will see more meaningful earnings fruition in the coming quarters (Kenanga Research). Exposure to Automotive is good due to high barriers of entry and stable recurring income.

Completion of Automation

According TA Research on 20 Apr 2017, MPI has completed its investments in vision inspection equipment. However, immediate cost savings are unlikely to be realised, as the 519 workers are redirected to different roles to support expansion plans. 4QFY17 capex is expected to be minimal.

Global Leader in MLP

MPI is among the top producers of micro leadframe package in the world. To grab more market share, MPI spending a lot in CAPEX and R&D to improve the features of its MLP as well as increased production efficiency through reducing floor space and headcount, and shortening assembly cycle time.

Exposure to Stable Automotive & Industrial segments

MPI has relatively larger exposure to the automotive and industrial segments as compared to its peers, growth in these segments is typically more stable over time because of longer product life cycles.

Margin Improvement

MPI has been targeting high-margin portfolios for leaded high-density packages, MLP, and test

services which contribute around 85% of sales.

Potential M&A

MPI is actively looking for automotive related acquisition targets to acquire technologies to expand its existing capabilities, which is in line with its plans to grow automotive segment. With net cash of RM419.7m, M&A related activities can be done easily.

Beneficiary of Depreciating Ringgit

Benefiting from stronger USD, although MPI typically hedges 50% of its net USD exposure 12 months forward. Sales are mainly denominated in USD, but only 50-60% of costs (mainly raw materials) are denominated in USD.

Source: AllianceDBS Research

WEAKNESSES & THREATS

Cyclical Nature of Smartphones & Tablets market

A major slowdown in the smartphones sales (possibly due to high market penetration), will hurt MPI, contribution from the smartphone segment is still significant at the moment (around 40%)

Sharp Depreciation of USD (which is unlikely)

Depreciation of the USD would affect its earnings as sales are mainly denominated in USD

Global semiconductor outlook

MPI is a general OSAT player but with a more diverse customer base, it does not have excessive exposure to a single large customer. As such, its fortunes are generally tied to the outlook for global semiconductor sales. Its price and valuation are affected by the performance of other listed OSAT players, which are mostly based in Taiwan (ermm, im not familiar with taiwan market).

Source: AllianceDBS Research

|

| for reference only, info outdated, cant get the latest at the moment |

--------------------------------------------------------------------------------------------------------------------------

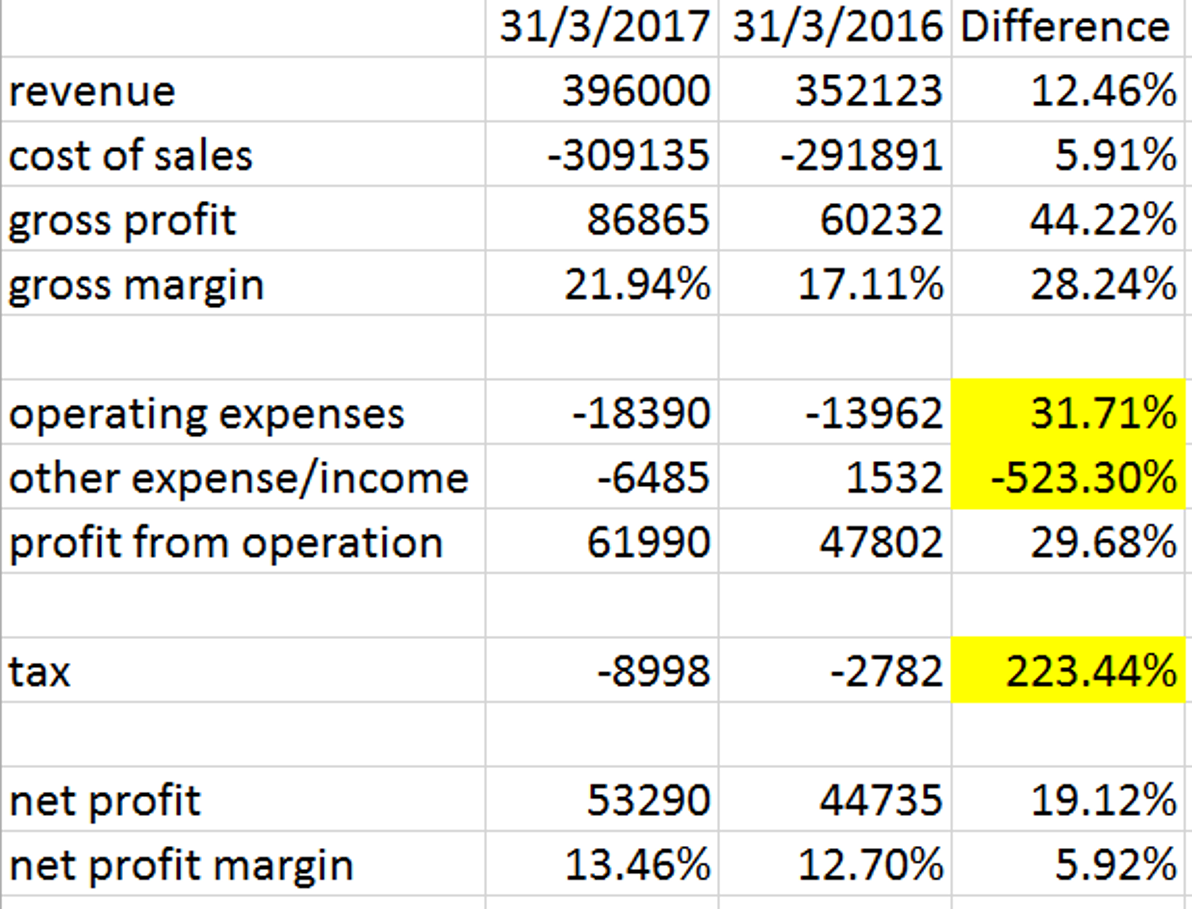

Profit increased substantially over the last 4 years in tandem with consistent growth of revenue. Profit margin has been improving over the years. High ROIC & ROE, high profit margin and is expected to improve further due to larger exposure to automotive and value added products, cash position is superb and dont have any long term borrowings as per Q3 report, with net cash of RM419.7m, acquisition related activities can be done easily. MPI is now trading at the acceptable EBIT multiple of 8.34 and P/E of 12.91.

According to projected earnings by TA Research, P/E of MPI for FY17=12.15, FY18=9.89, which is very attractive if and only if the earnings can be achieved :)

In a nutshell, MPI is expected to grow with in tandem with the recovery of semiconductor industry. Larger exposure to automotive is good due to high barriers of entry and stable recurring income, which can offset the cyclical nature of communication sector and decreasing demand in PC. Any automotive related acquisition would be great to boost its earnings to the next level. I will monitor closely on its automotive's revenue contribution as it is critical to its future growth. To me, the downside risk is limited, and im willing to buy more during weakness :)

Disclaimer: it is not a buying recommendation, your money, your decision

|

| source: http://www.malaysiastock.biz |

Profit increased substantially over the last 4 years in tandem with consistent growth of revenue. Profit margin has been improving over the years. High ROIC & ROE, high profit margin and is expected to improve further due to larger exposure to automotive and value added products, cash position is superb and dont have any long term borrowings as per Q3 report, with net cash of RM419.7m, acquisition related activities can be done easily. MPI is now trading at the acceptable EBIT multiple of 8.34 and P/E of 12.91.

According to projected earnings by TA Research, P/E of MPI for FY17=12.15, FY18=9.89, which is very attractive if and only if the earnings can be achieved :)

In a nutshell, MPI is expected to grow with in tandem with the recovery of semiconductor industry. Larger exposure to automotive is good due to high barriers of entry and stable recurring income, which can offset the cyclical nature of communication sector and decreasing demand in PC. Any automotive related acquisition would be great to boost its earnings to the next level. I will monitor closely on its automotive's revenue contribution as it is critical to its future growth. To me, the downside risk is limited, and im willing to buy more during weakness :)

Disclaimer: it is not a buying recommendation, your money, your decision