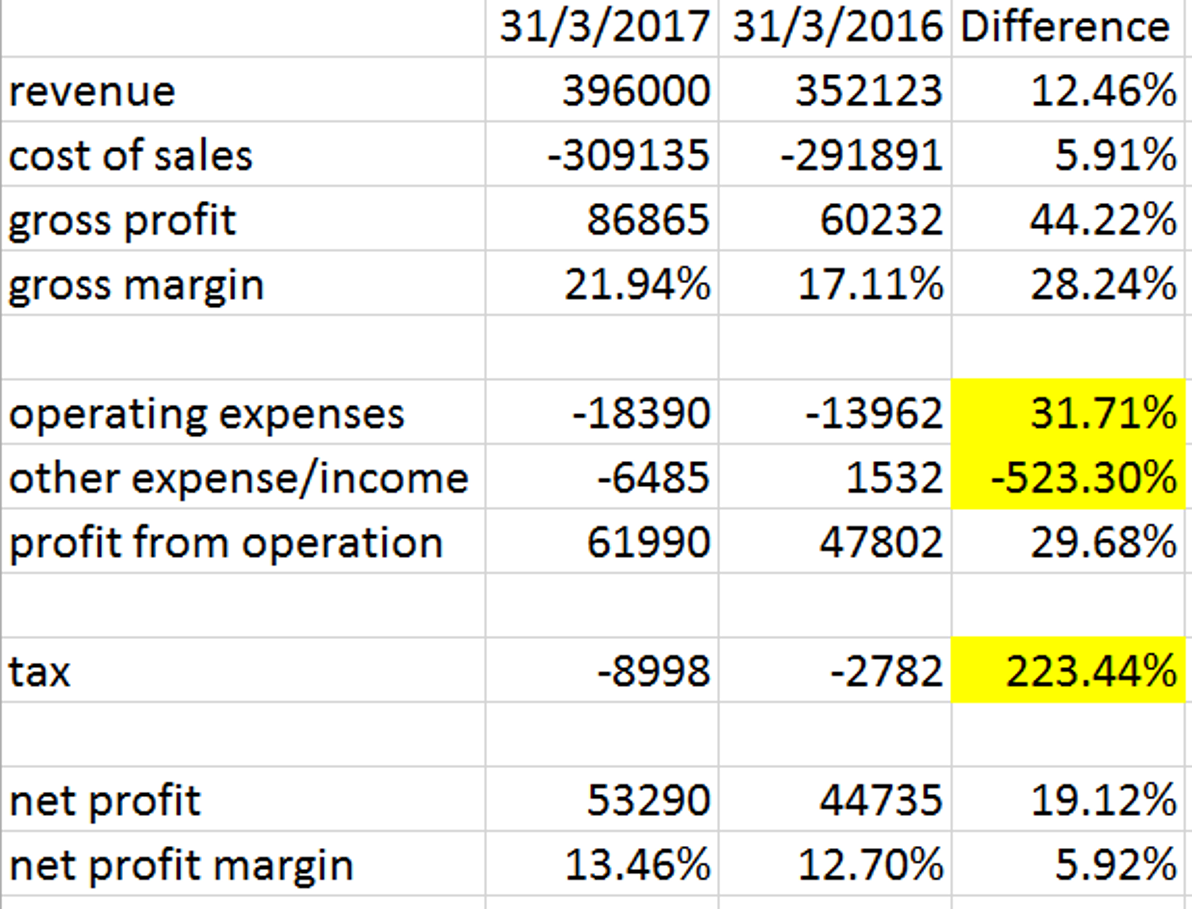

Revenue rose 12%, mainly due to higher contributions from Asia, US and Europe segments which climbed 7%, 28% and 10% respectively yoy. Gross profit and profit margin improved impressively as the cost of sales is well managed. Operating expenses are increased probably due to R&D. Other operating expenses increased substantially due to forex loss. Prior years' deferred tax resulted in big gap in taxation.

Prospects

The Board anticipates the industry to grow moderately in the coming quarters. Barring any unforeseen circumstances, the Board expected the performance of the Group to be satisfactory for the financial year ending 30 June 2017 (extracted from Q3 report).

Technical Outlook

MPI is now trading at the PE of 12.73, this is considered quite "cheap" in tech sector. MPI had surged 50% since the released of Q2 result, i managed to grab some at 10.82 during "promotion" last week. MPI is now trading at range of 10.75-12, immediate resistance at 12, i will add a little if it manages to break the resistance with high volume, but definitely not tomorrow, from what i learned from past experiences, a stock will normally close up sharply in tandem with the satisfactory result released the next day, but it could drop on following day because of profit taking.

i will write a detailed analysis on MPI and market outlook if time allows~~

Disclaimer: it isn't a buying recommendation, your money, your decision

Disclaimer: it isn't a buying recommendation, your money, your decision

No comments:

Post a Comment